Is SunPower a Better Buy Than First Solar?

Image Source: Pixabay.com

First Solar(NASDAQ: FSLR)and SunPower (NASDAQ: SPWR)are the two leading companies in the solar sector. Bothcompaniesbenefit from strong solar growth potential driven by system cost reduction and favorable policy initiatives. Because solar PV costs fall as solar cells become more efficient and governments grant tax breaks for renewables to combat climate change, SunPower estimates that total global demand for solar will almost double by 2020 to over 100 GW annually.

In terms of performance, First Solar has done better than SunPower. First Solar shares have advanced 13% over the past year, while SunPower has declined 30%. Given that past performance doesn't predict future returns, however, which company is the better buy moving forward?

First Solar and SunPower both have great balance sheets and a healthy yieldcoFirst Solar has $1.5 billion of net cash on its balance sheet, while SunPower has $1 billion on its balance sheet. SunPower has a parent in Totalthat owns the majority of the company and that could provide liquidity if SunPower's balance sheet deteriorates.Having a strong balance sheet is important, because it allows First Solar and SunPower to retain more value through yieldcos or holdcos without having to face the potential for a liquidity death spiral that SunEdison faced.

Both companies also own meaningful shares of their joint yieldco,8point3 Energy Partners(NASDAQ: CAFD). While the yieldco model has failed forTerraForm Powerbecause of liquidity concerns over its parent,SunEdison,the yieldco model is working for 8point3, as its dividend yield is low and the company is growing. Because it's dual-owned by First Solar and SunPower, 8point3 is also arguably superior than other yieldcos because there's lower potential for conflicts of interest given the dual ownership. Moving forward, 8point3's growth will provide First Solar and SunPower with a cheap source of capital and accelerate each company's growth.

SunPower has a higher earnings yield on an adjusted basisIn terms of GAAP earnings, First Solar has been more profitable. First Solar reported a GAAP EPS of $5.37 for 2015, good for an earnings yield of 7.8%, while SunPower reported a 2015 diluted GAAP loss of $1.39 per share, giving it a negative-6% earnings yield.

In terms of non-GAAP earnings, however, SunPower's earnings yield is better. Because of its accounting practices, First Solar's non-GAAP earnings would still be the same, while SunPower's non-GAAP diluted EPS was $2.17 per share for 2015, giving it an adjusted earnings yield of 9.5%.The main reason SunPower's non-GAAP profits are higher than its GAAP profitsis SunPower's accounting treatment of its dropdowns to the 8point3 yieldco. The different accounting treatment doesn't make SunPower less profitable.

The same holds true for 2016. First Solar expects to make a profit of between $4.00 and $4.50 per share for the year, giving it a forward earnings yield of 5.7% to 6.5%, while analysts expect SunPower to make a non-GAAP EPS of $1.95, good for an 8.5% forward earnings yield. (In terms of GAAP, SunPower management has guided for earnings of between $0 and $0.36 per diluted share for 2016.)

SunPower is growing faster and has more potentialSunPower plans to triple its capacity to 4 GW by 2019 from 2015 levels. First Solar, on the other hand, expects to ship2.9 GW to 3.0 GW for 2016, basically flat from 2015's shipment of 2.9 GW. In terms of future production guidance for 2017 and beyond, management has said it will provide more details during its Analyst Day on April 5.

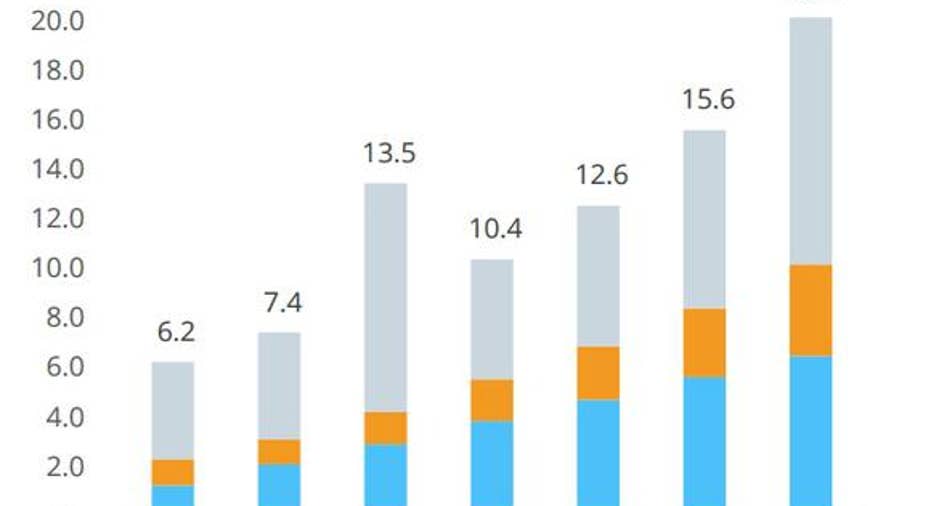

U.S. solar demand. Source: SunPower investor relations.

While both companies have differentiated technology, with First Solar using cadmium telluride and SunPower's panels being more efficient than the average, SunPower's technology is better because it gives the company an advantage in the fast-growing distributed-generation market, where space is limited. Because of falling solar costs, SunPower forecasts that the total U.S. demand for distributed energy will more than double to almost 10 GW a year by 2020 from 2015 levels.

SunPower's distributed generation division is growing quickly as a result. For the U.S. residential market, SunPower's installed leases jumped 60% year over year in the fourth quarter, and for commercial distributed generation projects, the company has a pipeline of $1.1 billion in bookings at the end of 2015. Because its technology isn't as efficient and its management hasn't made rooftop solar a priority, First Solar doesn't have much market share in the distributed-generation sector.

SunPower is the better buy Both First Solar and SunPower are great investing choices because each company will benefit from the ITC extension, the U.S. solar tariff on Chinese solar panels, and production cost declines going forward. While First Solar will be more GAAP-profitable in 2016, SunPower will be more non-GAAP profitable and will grow faster. SunPower also has a big advantage in the distributed-energy sector and arguably has more upside.

The article Is SunPower a Better Buy Than First Solar? originally appeared on Fool.com.

TMFJay22 has no position in any stocks mentioned. The Motley Fool recommends Total (ADR). Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.