Will I Have to Pay Medicare Premium Surcharges?

SOURCE: PIXABAY.

Medicare provides health insurance coverage to about 50 million seniors, and while Medicare Part A is free for most Medicare recipients, Medicare Part B, which covers things such as doctor visits, and Part D, which helps pay for medicine, charge recipients monthly insurance premiums. Because the government picks up a lot of the tab, premiums for Medicare Part B and Part D aren't very high for most people (relative to employer-sponsored health insurance). However, means testing can lead to surcharges that make plans far more expensive for higher-income Americans. Will you be among those who pay the surcharge? Read on to find out.

Digging into the detailsAmericans with high incomes are required by law to pay more for their Part B and Part D premiums, and while this rule affects only about 5% of Americans today, the number of Americans paying Medicare surcharges is expected to climb over the next decade because income levels used to calculate surcharges aren't adjusted for inflation

Typically, the government picks up 75% of the cost of Medicare Part B and recipients pay the rest. High-income beneficiaries, however, pay 35%, 50%, 65%, or 80% of the cost of Medicare Part B, depending on their modified adjusted gross income (MAGI), or adjusted income plus tax-exempt interest income.

The percentage high-income earners pay is determined by a sliding scale that's applied to the MAGI listed on your most recent federal tax return. In 2016, individuals and couples filing jointly with MAGI's above $85,000 and $170,000, respectively, will pay a greater share of their Part B and Part D premiums.

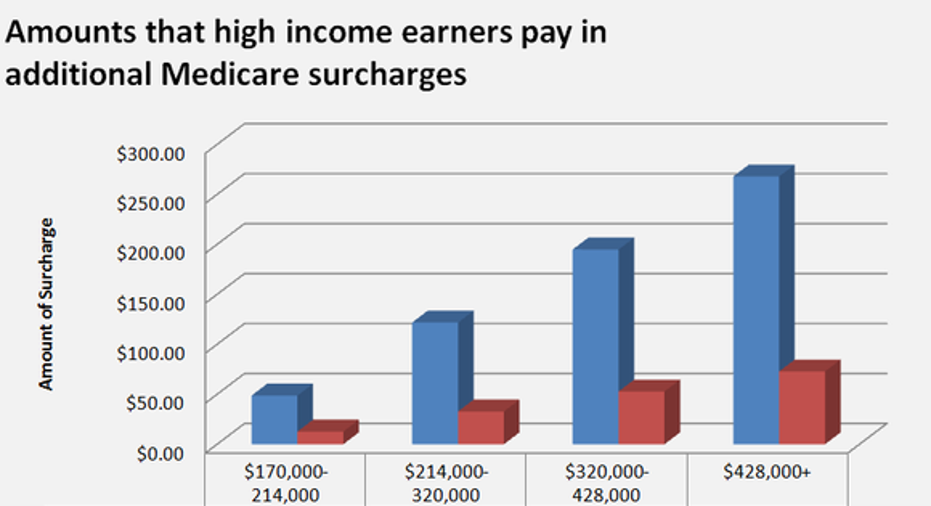

In 2016, the standard Part B premium paid by Medicare recipients is $121.80, and married couples with income between $170,000 and $214,000 will pay that, plus an additional $48.70 monthly surcharge. Couples with MAGI between $214,000 and $320,000 will pay the standard premium, plus $121.80, and those on the hook for the biggest payment are couples earning more than $428,000. They'll pay the standard premium, plus $268 per month, which works out to more than three times the premium the typical American pays.

Part D surcharges also increase with income, but because part D programs are offered through private insurers, their standard premium varies. Similar to Part B premiums, individuals and couples with MAGI above $85,000 and $170,000, respectively, will pay whatever their insurer charges in monthly premiums and a surcharge.

The following graphic shows exactly how much more high income couples will pay for Part B and Part D.

SOURCE: SOCIAL SECURITY ADMINISTRATION, AUTHORS CALCULATION.

Although the amount of your Medicare surcharge is calculated using your prior year's tax form, don't worry that you'll get hit hard by the surcharge in your first year of retirement. If your income drops substantially because you or your spouse stop working (or become part-time), contact Social Security and provide it with a letter from your employer regarding your retirement. Depending on your situation, it'll adjust what you have to pay. Similarly, if you get married, divorced, or become widowed, and that significantly reduces your income, you should contact the agency, too.

Tying it togetherAccording to HealthView Services, a 65-year-old couple retiring in 2015 and having income in the top Medicare bracket will pay $279,377 in Medicare surcharges over its lifetime. That's not chump change. Also, just because your income doesn't put you over the income limit today, that doesn't mean you couldn't still be at risk in the future. HealthView Services estimates that unless laws are changed to tie income limits to inflation. a quarter of all Medicare recipients will being paying surcharges by 2036. Given those odds, people in their 40s may want to factor surcharges into their retirement savings plans sooner rather than later.

The article Will I Have to Pay Medicare Premium Surcharges? originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.