4 Reasons This Is the Perfect Dividend Stock to Own During the Oil Crash

Source: Kinder Morgan.

The worst oil crash in half a century has laid bare the painful truth that high yields come with high risk and income investors who choose yield over quality do so at their peril. Take, for example, the case of two of America's largest pipeline blue chips, Kinder Morgan , and Enterprise Products Partners .

Over the past year, Wall Street has punished both severely. However, Kinder Morgan's collapse, while well earned (its mountain of debt forced management to slash the payout to fund growth projects), Enterprise Products Partners is a classic case of a market overreaction.

Let's examine Enterprise Products Partners' full-year 2015 earnings results to see just why this midstream MLP represents one of America's highest quality high-yield dividend growth stocks. More importantly, here's why Enterprise is so well positioned to protect and grow its payout in a world of lower energy prices.

Business model that's all about stabilityThe basis of the midstream MLP business model is a tollbooth-like river of cash flow ensured by long-term contracts. Both Enterprise Products Partners' and Kinder Morgan'scontract mix takes this basic premise and improve upon it via many oftheir contracts guaranteeing a minimum operating margin for use oftheir highly diversified assets.

Specifically I'm referring to Enterprise's focus on several key types of energy pipelines including: natural gas, crude oil, petrochemicals and refined petroleum products, and natural gasliquids (NGLs). Meanwhile Kinder Morgan has its hands in natural gas pipelines, LNG exports, CO2 distribution, oil tankers, and even oil production.

Why is this so valuable to dividend investors? Because while low oil and gas prices may decrease oil and gas production (so-called "supply push" volumes), very low gas and NGL prices can provide volume protection because demand from oil and gas customers ("demand pull" volumes) can offset this.

This providesboth Enterprise Products Partners' andKinder withdistributable cash flow (DCF) -- which iswhat's neededfor the sustainable and steady distribution increases -- withincredible stability despite oil prices collapsing 70% since their mid-2014 highs. For instance, in 2015 Enterprise's cash flow (excluding asset sales) increased 2.5%, quite impressive given the carnage of the current energy markets.

BUT if Kinder's DCF is also stable then why is Enterprise in a better position? Because of three other factors that make Enterprise Products Partners far superior to Kinder Morgan.

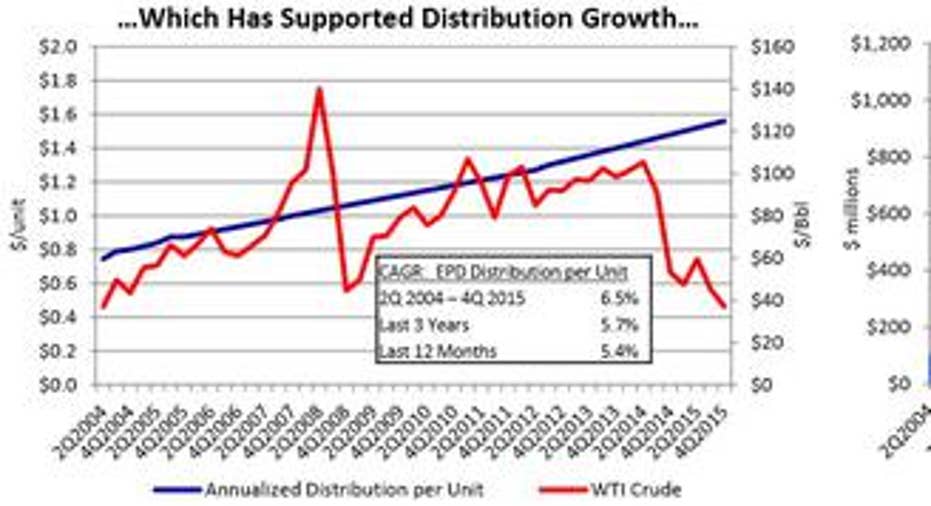

Payout profile that can withstand almost any storm

Source: Enterprise Products Partners investor presentation.

These images illustrate Enterprise's two largest competitive advantages, and why its such a superior choice to rivals such as Kinder Morgan.

Whereas other pipeline operators, suchas Kinder Morgan before its 75% dividend cut,were focused on growing their payout as quickly as possible at the expense of retaining almost no DCF, Enterprise Products has always emphasized slower, but far steadier, payout growth.

This focus on a high ratio of retained DCF, even during the oil boom times, has created a vast excess cash flow cushion that allows Enterprise to continue raising its payout when most of its peers arejust maintaining, or, like Kinder, slashing theirs.

In fact, in Q4 2015, the MLP announced its 46th consecutive quarterly payout increase. What's more, management even issued 2016 distribution growth guidance predicting 5.2% growth,resulting ina generous forward yield of 7%.

Large growth opportunities, and most importantly ...Investors should never simply accept management guidance as gospel. Rather, you should require evidence that 2016 willprovide some kind of growth catalyst that will result in DCF growth sufficient to sustainably achieve the MLP's payout growth target.

In this case, Enterprise's growth will probably becourtesy of $4.5 billion in new projects that are coming online.

Source: Enterprise Products Partners investor presentation.

Of course, planned projects need to be funded, and that is where another Enterprise Products Partners' strength lies -- inthe form of$4.4 billion in available liquidity as of the end of 2015.

... plenty of access to cheap capital to execute on itWith financial markets in a near panic over the threat of energy defaults, Enterprise Products Partners' annual excess DCF of over $1 billion per year is a godsend that helps it to fund a significant portion of its growth internally. Not only does that result in a much lower leverage ratio than rivals such as Kinder Morgan (which is partially why Enterprise has the highest credit rating in the industry at BBB+), but it also minimizes the need to raise equity funding by diluting current investors with a rising unit count.

That in turn helps keep the long-term coverage ratio high and makes further steady payout growth much more likely to continue even if energy prices remain low for several years.

Bottom lineThe sadstory of Kinder Morgan's dividend cut should serve as a cautionary tale that shows the importance of long-term investing principles. Specifically, the dangers offocusing primarily for short-term yield and payoutincreases rather than long-term distribution security and steady growth.

With Enterprise Products Partners, income investors have the opportunity to invest in one of the industry's best-managed midstream MLPs, and at valuations that not only lock in a generous current yield but is alsolikelyto result in market-crushing total returns in the years ahead.

The article 4 Reasons This Is the Perfect Dividend Stock to Own During the Oil Crash originally appeared on Fool.com.

Adam Galas has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Kinder Morgan. The Motley Fool recommends Enterprise Products Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.