3 Stocks to Consider Buying Near 52-Week Lows

Finding value stocks in a market near all-time highs can be challenging. And it often means investing against the conventional wisdom driving the market higher. In today's market, looking for value means looking past the shiny, high-growth tech stocks to some slower growth and maybe more traditional companies.

The three that caught our eye this week are Covanta Holding Corp (NYSE: CVA), International Business Machines (NYSE: IBM), and Nike (NYSE: NKE). Here's why their lows are buying opportunities for long-term investors.

Image source: Getty Images.

No end to the trash

Reuben Gregg Brewer (Covanta Holding Corp): Covanta Holding Corp is within 10% of its 52-week low and yields an impressive 7%. Those two facts easily put it on the radar screen for income investors seeking bargains. Now add in a unique approach to a boring, but necessary, business and Covanta's low price looks pretty enticing.

Covanta is a trash company (70% of 2016 revenues), but unlike larger peers such as Waste Management, it burns the garbage it collects to generate electricity (22%). It also generates revenues from recycling (3%). This provides the company three different ways to benefit from the trash it collects, with roughly 85% of its trash business under long-term contracts and nearly 90% of its electric generation contracted or hedged.

The problem for Covanta of late has been the expiration of long-term contracts signed at higher than market rates. That period of adjustment is nearly over, but the last few months have seen two notable fires at company facilities that will likely hamper near-term results. Add in expansion projects in Europe and a heavy debt load (long-term debt is roughly 70% of the capital structure) and you can see why investors are worried.

However, Covanta operates in a necessary business with a contract-protected revenue stream. It can handle a relatively heavy debt load. Moreover, the shares are likely to rebound as Covanta works through the fires and expands further into Europe. There's risk here for sure, but the potential rewards appear substantial... including being able to collect a hefty yield while you wait for a rebound.

A bad start to the year

Tim Green (International Business Machines): After soaring in 2016 and early 2017 on optimism that its turnaround was finally making progress, shares of IBM have stumbled. The company's first-quarter report was a disappointment, with revenue coming in below expectations, and news that Warren Buffett had sold a significant portion of his massive stake in the company added salt to the wound. IBM stock is now close to its 52-week low, presenting investors with an interesting opportunity.

IBM expects to produce adjusted earnings of at least $13.80 this year, putting the PE ratio at a measly 11. A dividend yield of nearly 4% sweetens the deal, making the stock tempting for investors looking for value in an expensive market. Some things are going right for IBM: the cloud business is booming, bringing in $14.6 billion of revenue over the past year, and the growth businesses now account for 42% of total sales. But the inflection point where revenue begins growing again has yet to be reached.

It's unlikely that the market will give IBM credit for its transformation without a return to revenue growth, so the stock may be stuck in the doldrums until then. That point may come later this year, when IBM is expected to launch a new mainframe that will drive a spike in hardware sales from existing customers. But a return to sustainable revenue growth may be further off, with shrinking legacy businesses still dragging down the top line. For investors with enough patience, IBM is a stock to consider.

The future of retail

Travis Hoium (Nike): At a time when the stock market is near an all-time high, it's strange that one of the most successful companies over the last four decades hasn't followed suit. But Nike is hovering just a couple of dollars above its 52-week low, and doesn't show any signs of picking up any steam.

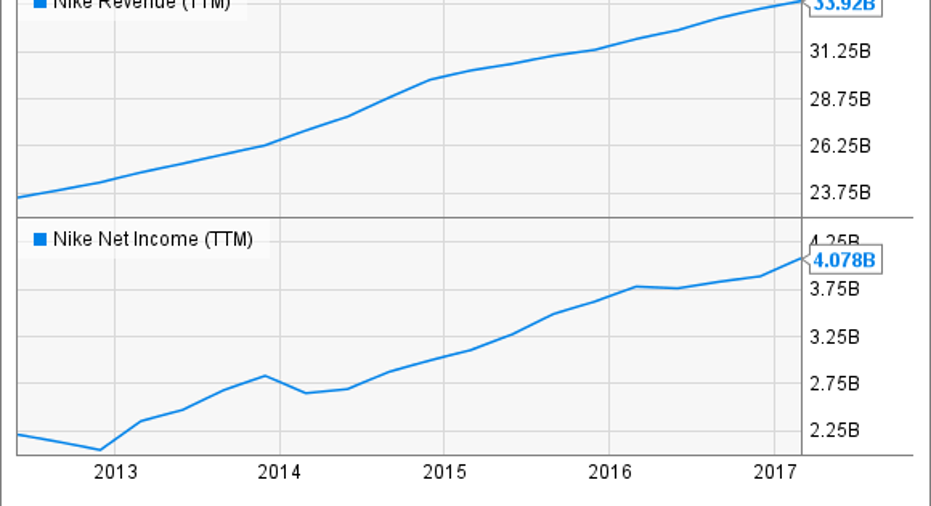

The problem hasn't been with Nike's fundamentals. You can see below that the company's growth has stayed strong in recent years, and net income growth is outpacing revenue.

NKE Revenue (TTM) data by YCharts

The market may be more enamored with companies in tech that have near infinite growth opportunities, but Nike is as well positioned in retail as anyone. Nike has embraced the showroom retail concept more than most brands with its own retail presence. And digitally it's embracing marketing strategies that allow it to reduce overall channel inventory, expand margins, and obtain more knowledge about customers.

Long-term, buying Nike at the 22 P/E ratio that shares trade at today could look like a real steal. The company has a dominant brand and is embracing strategies that will allow for growth, even as the retail landscape changes. For investors looking at stocks near 52-week lows, this is a great pick.

10 stocks we like better thanWal-MartWhen investing geniuses David and TomGardner have a stock tip, it can pay to listen. After all, the newsletter theyhave run for over a decade, the Motley Fool Stock Advisor, has tripled the market.*

David and Tomjust revealed what they believe are theten best stocksfor investors to buy right now... and Wal-Mart wasn't one of them! That's right -- theythink these 10 stocks are even better buys.

Click hereto learn about these picks!

*StockAdvisor returns as of May 1, 2017The author(s) may have a position in any stocks mentioned.

Reuben Brewer owns shares of IBM. Timothy Green owns shares of IBM. Travis Hoium has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Nike. The Motley Fool has a disclosure policy.