Qorvo's Big Problem: Relying Too Much on a Few Customers

Qorvo's (NASDAQ: QRVO) latest earnings report continues to show a company that is highly dependent upon a handful of customers. If something goes wrong at one of these companies Qorvo's results can be negatively affected, which would provide a headwind for the stock.

Image source: Qorvo

A quick look at the quarter

Qorvo finished the third quarter of its 2017 fiscal year on Dec. 31. Below is a year-over-year comparison to last year's Q3 and guidance for the fourth quarter compared with actual numbers from last year's Q4..

| Metric | Q3 2017 | Q3 2016 | Year-Over-Year Change | Q4 Guidance | Q4 2016 | Year-Over-Year Change |

|---|---|---|---|---|---|---|

| Revenue | $825.4 million | $619.7 million | 33% | $610 million to $650 million | $607.1 million | 3.77% at midpoint of guidance |

| Gross margin | 44.3% | 47.9% | (3.6 percentage points) | 46% | 50% | (4 percentage points) |

Data source: Qorvo.

Based on Qorvo's guidance, at the midpoint, the company will only achieve 3.77% non-GAAP year-over-year revenue growth in the fourth quarter and see operating margin decline by 400 basis points. President and Chief Executive Officer Bob Bruggeworth said in his prepared remarks accompanying third-quarter results that the "greater than historical sequential decline" is forecast "as two of our leading customers inChinaand a tier-one customer inKoreadelay flagship smartphone launches."

Looking back to last year's annual report from May 2016, remarks by Bruggeworth in the shareholder letter had a similar theme: "Mobile revenue grew at levels below our expectations, primarily due to softness in China in our September quarter and weaker than forecasted demand from a large marquee customer later in the year, which negatively impacted what is usually the strongest period of smartphone sales.

Qorvo's markets

Qorvo breaks its business down into two major categories. Mobile products consists of a variety of analog devices that go into mobile devices, including smartphones, notebook computers, wearables, tablets and cellular-based applications for the Internet of Things. Infrastructure and defense products consists of analog devices for cellular base stations, optical long haul data centers, switching networks, Wi-Fi and cable networks, connected cars, and the home automation market, as well aerospace and defense applications.

It is important to note that in the third quarter, 80% of Qorvo's business was derived from mobile products. The company is highly dependent upon the needs of the smartphone market that drives the bulk of its mobile products revenue.

Customers and margin pressure

Qorvo cites three major customers that accounted for more than 50% of the company's revenue for the past two years and 49% in 2014. One of the customers remains unidentified by the company and Qorvo sells its products to that company through multiple contract manufacturers. (RF Micro Devices Inc. and TriQuint Semiconductor Inc. merged on Jan. 1, 2015, to create Qorvo Inc. The historical numbers reflect the combined business of both companies with the three customers.)

| Year | Customer A | Huawei Technologies Co. Ltd. | Samsung Electronics, Co., Ltd. | Total |

|---|---|---|---|---|

| 2016 | 37% | 12% | 7% | 56% |

| 2015 | 32% | 7% | 14% | 53% |

| 2014 | 20% | 4% | 25% | 49% |

Percent of total revenue from Qorvo's top three customers.Data source: Qorvo. Chart by author.

Being highly dependent on such few customers poses two major problems for Qorvo. As evidenced by Bruggeworth's remarks, the company is at the mercy of the performance of its large customers. If there is an execution failure on the part of the customer or another supplier to the customer's supply chain, Qorvo can be negatively impacted. The second problem is related to Qorvo's operating margin. Semiconductor OEMs typically receive a lower price for higher volume orders. This sets Qorvo up to be on the losing end of a customer being able to extract a low price from the winning bidder. Unless Qorvo can come up with products that other companies such as Skyworks Solutions, Inc. or Broadcom Limited cannot match, it will always face tremendous margin pressure from the OEM.

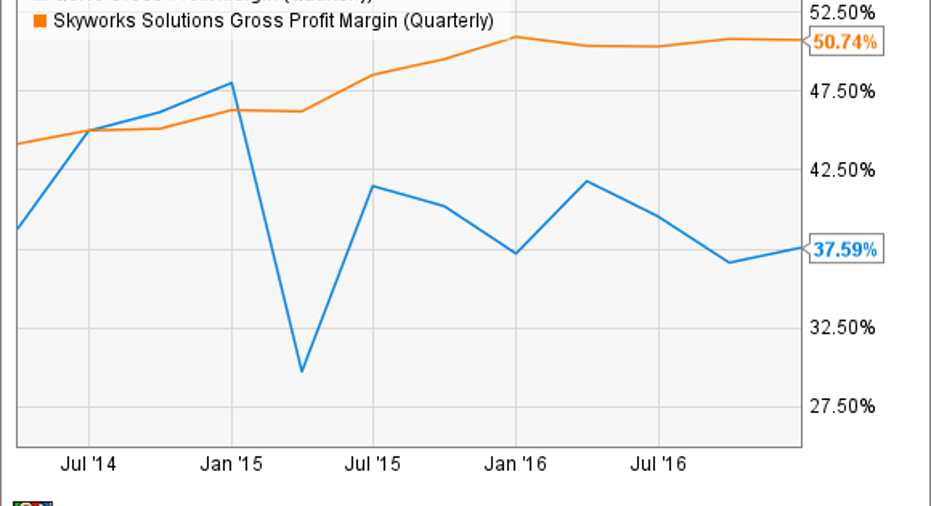

The other troubling factor for Qorvo is that its operating margin does not compare well to Skyworks', although they both compete in the same industries. Skyworks reports that it received 44% of its revenue from one customer in 2015.

QRVO Gross Profit Margin (Quarterly) data by YCharts

Qorvo's results demonstrate the risk when a company's revenue is highly dependent upon a small number of customers. The company's gross margin can be an indicator that it does not have pricing power with its key customers and as a result may not be able to produce the earnings required to drive its stock price higher.

10 stocks we like better than Qorvo When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Qorvo wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Frank DiPietro owns shares of SWKS. The Motley Fool owns shares of and recommends SWKS. The Motley Fool has the following options: short August 2017 $87 calls on SWKS and short August 2017 $85 puts on SWKS. The Motley Fool recommends AVGO. The Motley Fool has a disclosure policy.