2 Factors That Will Make or Break Ford Motor Company's 4th Quarter

Ford Motor Company Corporate Headquarters. Image source: Ford Motor Company.

Ford Motor Company (NYSE: F) is putting the finishing touches on its fourth-quarter and full-year earnings presentations, which are due out on Thursday January 26, 2017. When it's all said and done, 2016 will go down as one of the automaker's best years in company history, even if it falls slightly short of 2015's strong result. Let's take a look at guidance, what could make or break the fourth quarter, and where Ford is headed this year.

What to expect

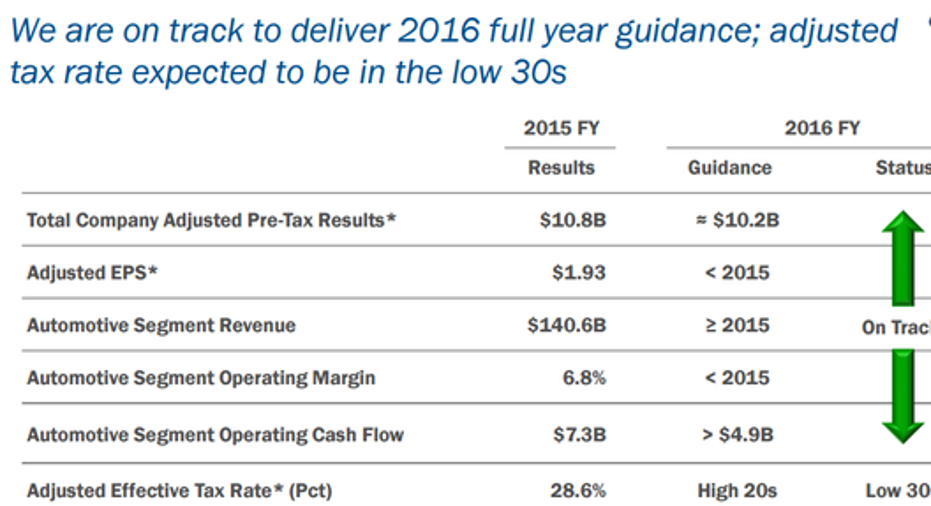

According to analysts' expectations, Ford's top line is expected to check in at $35.1 billion. That result would be down slightly from last year's $37.84 billion. Consensus estimates for the company's earnings per share are $0.32, which would be well below last year's $0.58 per share. Here's a look at Ford's guidance on a number of other metrics, compared to 2015.

Image source: Ford Motor Company'sDeutsche Bank presentation.

For the most part, investors know what to expect from Ford's North American region: the vast majority of company profits. But two things that could make the difference in the quarter will be Ford's results in Europe and with its finance division, Ford Credit.

Make or break

As new-vehicle sales slow in the United States, it's becoming more important for Ford to develop a second pillar of profitability to help offset slowing growth here. On a positive note, trends in Europe are increasingly favoring profits. Ford's sales in Europe moved 5% higher in 2016, to nearly 1.4 million vehicles, but sales of SUVs increased 31% last year.

In addition to accelerating SUV sales, nearly 60% of Ford's passenger car sales in Europe last year were high-series trims, including Titanium and Vignale, which are more profitable models. "Customers appreciate the enhanced performance and style in our high-series models," says Roelant de Waard, vice president of marketing, sales, and service for Ford of Europe, in a press release. "We are excited to launch the next-generation Fiesta with Titanium, Vignale and ST Line editions coming this summer."

Europe is more of a wildcard this quarter than usual, thanks to the U.K.'s decision to leave the European Union. Over the summer, Ford noted that Brexit had already cost the company $60 million due to the pound's decline and expects to lose roughly $200 million in Europe due to the development in 2016 and more than double that amount in 2017.

Sales haven't been as negatively impacted, at least so far, as many initially expected, and if automakers were overdramatic about costs, Europe could turn in a better bottom line than expected -- and that would be a big win for Ford during the fourth quarter.

Used-car woes

Many investors don't give enough credit, no pun intended, to Ford Credit. During the third quarter, it generated $552 million in pre-tax net income, higher than Europe and Asia-Pacific regions combined -- and those are Ford's two most profitable markets outside of North America. However, as a slew of used vehicles come off lease and are returned, if residual values continue to decline, it's going to pressure Ford Credit's bottom line. In fact, Ford already shaved $300 million from Ford Credit's full-year guidance.

The way it works is that Ford Credit will estimate the value of its vehicle when the lease is signed, and if it comes back less valuable than it expected, it quickly erodes the bottom line. Unfortunately, the National Automobile Dealers Association index of used-vehicle prices declined in each of the past six months of 2016 and dropped roughly 4% from 2015's average. That's the first significant decrease since the recession. Furthermore, the average used car depreciated about 23% during 2016, faster than the typical 18%.

Ford has already begun pulling back the percentage of total vehicles that it leases. During the fourth quarter, it leased just 19% of its U.S. vehicles, down from the 26% it leased during the first quarter of 2016 and much lower than the industry average, which is around 30%.

Ford's likely to put up another strong quarter for adjusted EBITDA, capping off another solid year, but whether or not the results top estimates is going to come down to how the company performed in Europe and how a flood of off-lease vehicles impacts Ford Credit's bottom line.

10 stocks we like better than Ford When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Ford wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Daniel Miller owns shares of Ford. The Motley Fool owns shares of and recommends Ford. The Motley Fool has a disclosure policy.